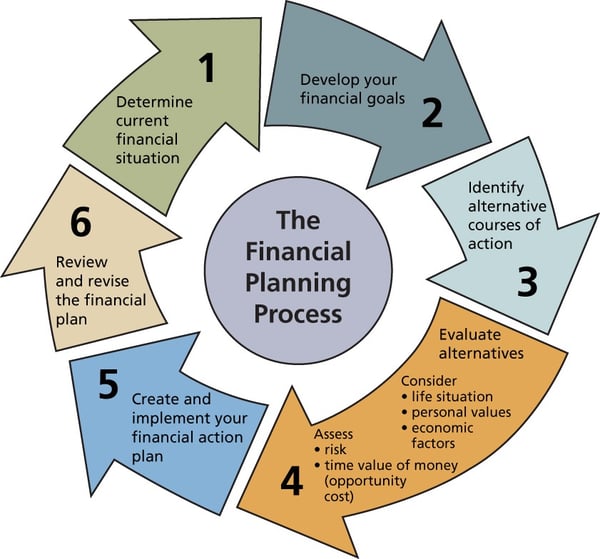

For many of us, the first quarter of the year is planning and preparing time. It’s time for us to review last year’s financial reports, analyze our position, strategize, and set goals. We consider how we can, over the next year, make better use of our resources, cut costs, gather better data, and, most importantly, grow.

While not all paths to growth will look the same as there are so many variables that can be different from one farm operation to another, the strategies and tools for growth are similar.

Quick Links

What are Your Growth Goals for the New Year?

Many of us have heard and read countless speakers and articles discussing setting goals. From S.M.A.R.T goals to data driven goals, regardless of the framework, the general consensus and understanding is that growth and change are led by the setting of the goals themselves.

So, what are your growth goals? For most farms, these can be broken down into three distinct areas: personal, production, and overall business goals.

Personal goals may include acquiring a valuable skill set for the farm operation (like accounting) or increasing individual equity in an operation.

Production goals may include improving crop yields, growing a herd or increasing output from existing livestock.

Business goals may include expanding operations to expand an existing profit center or even acquire a new one. It may include buying more land or more infrastructure to bring production or operations to a new level.

The primary factors to remember are that the goal should be directional in that it should move you in the direction you want to head. You may not get there all in one year, but by determining your direction, you can establish your course with smaller, S.M.A.R.T. goals.

And, to build out those goals, you’ll want to rely on the data you have at hand, or set a goal of gathering the data you will need to make strategic growth decisions.

Farm Growth Strategies

As we discussed in our blog on farm financial guidelines, one of the best tools we have at our disposal is our network, is other other farms, the operations we aspire to be like. By examining and comparing our reporting, we can better understand and analyze our position. Similarly, through exploring the strengths and weaknesses, the strategic moves and methodologies of successful farm operations, we can learn how to apply their successes to our own farms and ranches.

What do top producers have in common?

Everyone wants to be the best, do their best. You do not farm with hopes to fail. Unfortunately, some do fail, operations go under and are sold all of the time. Many of those owners are left wondering what they could have done differently to keep their operation afloat. While not all of those operations were salvageable, some could have probably been helped along by just implementing a few of the same practices that the top ag producers have implemented in their own operations.

Having goals, having a strategy, having contingency plans, having the tools to make quick decisions, the courage to say “This is not working” and seek out a solution, the drive to keep learning, and the humbleness to say “I don’t know, but there is someone out there who does.”

Those are a few of the things top producers have in common that make them successful. In fact, at our yearly user conference we often invite guests who have a demonstrated history of finding growth and success. A few of our favorites from the past include:

- Danny Klinefleter, Texas A & M University-Twelve things that 98% of Commercial Ag Producers don't do

- Dick Witman, financial consultant-Next Steps in Implementing Ag Management Accounting

- Daryl Ellis, financial consultant-FBS Report Levels & Reporting Implications

And, when it comes to making those smart moves, they’ll all tell you there are 3 important elements to achieving the level of farm management and growth you aspire to.

Key Elements to Farm Management and Growth

In any business you have to have a strategy. Farms, of any size, are a business and so strategy should be laid out. Often, especially in the case of family farms, it’s easy to forget it’s also a business and so strategy discussed over the kitchen table isn’t the same as having it on paper. In your head or casual discussions are not enough. Map it out.

In fact, you may already be employing strategies on your farm. You’ve likely got a crop strategy or maybe a livestock strategy. A financial strategy simply ties it all together.

Your financial strategy is also your budget. Budget for inputs, budget for expected harvest (crops or livestock), budget for expansion and have contingency budgets if things don’t go as planned.

These strategies or budgets help you anticipate what is ahead for your operation.They also allow you to adapt to changes: financial, weather, market. Most importantly, they allow you to capitalize on these changes in a quick and concise manner. Those who are able to adapt and make decisions quickly are more likely to see greater returns on their decision.

To be a top producer you need to be willing to take risks. If you have your strategy and contingency strategy mapped out, you take some of the danger out of that risk.

2. Knowledge is Key

Once you have a plan, you need to be able to implement it. Some of the initiatives and plans you have mapped out may mean stretching beyond your comfort zone. It might mean learning something new (check out the Financial Guidelines for Agriculture: An Implementation Guide for Non-Accountants).

Still, it means understanding what farm information you have at this time and what information you still need. That may mean investing in a farm ERP solution that helps you aggregate data or it might mean educating yourself.

In this case, investing in yourself is investing in your business. There are several ways to do this. You can attend conferences, training, or classes.Talk to peers who are doing what you want to be doing and be a sponge soaking in their knowledge. Don’t be afraid to admit when something is beyond your ability as we all have strengths and you may be able to exchange expertise.

For example, your specialty might be the grain side of the operation, but the financial side makes your head spin! Learn as much as you can about the financials but realize your limitations and lean on experts when you need help. They can be agricultural accountants, nutritionists, crop advisors, CPAs, CFOs, or even something like data entry- you don’t have to be an expert in that area to hire the expert to help you.

3. Financial Statements

Once you have your strategy and the people in place to implement the strategy, you need to monitor the results. Top producers are able to have real time data at their fingertips to monitor progress and results and that means financial reporting.

Top producers have accrual financial statements to show them what their costs (margin) are and what their managerial costs are. You must be able to monitor your actual performance against your budget and adjust accordingly.

Having this information allows you to say, "well things aren’t going as planned, so now is the time to cut losses." The ability to look at financial statements in real time to see where you stand in time to change strategies and the willingness to make that decision to stop what you are doing and go in a different direction is key.

The verse “Pride goes before destruction, and haughtiness before a fall” (Proverbs 16:18) says it all. Sometimes you have to take your pride out of the equation and admit something is not going to work to keep your operation from destruction. When you have the numbers that don't lie in front of you they make the decision for you. Pulling the plug on your idea when it isn’t going as planned is hard, but essential.

While the biggest tool you can possess is you– your attitude, willingness to try, your willingness to learn and not give up– there are other tools that can help. Software like FBS Systems integrated managerial accounting software will get you the accrual financial statements you need and help you plan, budget, and report as needed.

If you’re ready to talk about how we can help, reach out to us today and let’s get started building your strategy and implementing the tools that will help see it to fruition.