Farming is about growth. It’s the primary focus from crop and livestock to the back office. Crops don’t grow from seed without external factors, nor does livestock. So how can we hope for our overall farm or ranch operation to grow without considering all the growth factors that allow the business side to thrive or wither?

And, when we see a challenge or opportunity to address a production shortfall, we look at all the options on the table. The growth path decision tree applied to farm accounting allows us to do the same. We look at the accounting decisions that impact our decision making process and assess how we can use accounting methods to improve our operations and profitability.

Quick Links

- What is Growth Path Accounting?

- What is Method B Accounting?

- Challenges of Method B Accounting

- Benefits of Method B Accounting in Farm Accounting

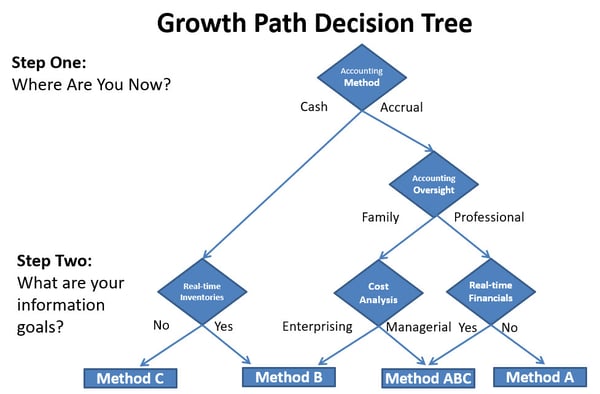

What is Growth Path Accounting?

In simplest terms, growth path accounting enables you to increase your accounting knowledge and, as a result, have greater control over your financial future.

When computers first became a farm tool, surveys revealed many believed that accounting was their computer's most important function. Unfortunately, for many, selecting the right farm accounting system has been a hit-and-miss exercise.

First introduced in the FarmSmart newsletter way back in 1985 and updated since then, Growth Path Accounting provides farm managers with step-by-step procedures for selecting and maintaining their farm accounting system.

The Growth Path concept assumes that:

- Farmers may not have an accountant on staff and, individually, have varying levels of accounting experience and time available for bookkeeping.

- Each farmer's information goals are as unique and constantly changing as his farm business.

- Farmer-accessible education and training, regarding agricultural accounting, are both scarce and expensive.

Each farm accounting method presented in Growth Path Accounting results in different outcomes and so understanding each method is key to making the right choice.

What is Method B Accounting?

Method B accounting is sometimes referred to as the “farmer’s shortcut” as this hybrid approach to farm accounting provides a shortcut to track inventories and generate cost analysis reports and closeouts.

Method B is best used in two scenarios.

The first scenario is if you're strictly using cash accounting but want to incorporate real time inventories of crops, livestock, or inputs.

The second scenario is if you're primarily accrual and want to add some form of enterprise cost analysis that exceeds the scope of your existing accounting system or if you do not have a formally-trained accountant on staff.

Method B includes:

- Integration with production information. If you're tracking field or livestock performance records, the direct and indirect costs will come through your farm accounting records.

- Cash and/or accrual accounting. You can continue using your current accounting method. Financial statements will not be affected.

- Real-time inventory tracking. Both farm accounting and production events will drive inventories. Inputs like seed, chemicals, fertilizer and feed will be valued at cost from accounting while growing/harvested crops and growing animals can be assigned either standard costs or market values.

- "Hybrid" approach that maintains "pure" cash and/or accrual accounting books but also does enterprise analysis and inventory "on the side" through specialized reports that merge accounting and production data.

What Are the Challenges of Method B Accounting?

Every farm accounting method has potential advantages to improve your overall outcomes. However, one of the things that holds true of any accounting method, especially when it comes to the complexities of farm accounting, is that it also comes with challenges. Method B is no exception. Some of the challenges include:

- Users will need to make manual accounting adjustments to reverse prepaid expenses in cash accounting and cost of goods sold for accrual accounting systems.

- Cost allocations and inventories do not "drive" financial statements through raw materials, work in process, and finished goods inventories. Overhead allocations are also limited to a "single hop" (rather than service centers allocated to support centers that are allocated to production centers).

- Limited accounting control because physical inventories don't tie to financial statements.

- Doesn't follow Generally Accepted Accounting Principles (GAAP).

What are the Benefits of Method B Accounting?

Even with those challenges, many of those issues are fairly standard for farm accounting. It’s likely nothing you haven’t seen before. So the true choice lies in understanding how Method B can benefit your farm or ranch’s overall financial operations and success.

In many ways, Method B simplifies operations and data acquisition for financial purposes. The benefits include:

- It can produce unit-based cost analysis and inventory control with much more detail and automation than Methods A or C.

- No additional accounting training required as analysis reports do not tie to financial statements.

- Handles all data integration functions "behind the scenes."

- Doesn't require that production employees allocate costs or accounting employees track production details.

Many FBS Systems users rely on Method B as a shortcut, but it’s worth noting that Method ABC, another branch to the growth path, doesn't compromise accounting practices or business analysis.

Regardless of the farm accounting method that works best for you, the key piece is staying flexible and leveraging all the data available to you. Growth and the strategies that lead to growth must always be informed decisions. That means finding the right balance of field and office as well as a way to integrate the two.

The best option to do that is a farm ERP solution like the one offered by FBS Systems. If you’re ready to talk about how we can help you leverage data from across your organization, streamline your accounting, and develop forward thinking strategies for growth, reach out to us today. We’d love to show you what we can do!